The Contemporary Art Market 2024/25

Adjustment, Not Collapse

After the exuberance of the post-Covid years, the contemporary art market has entered a phase of recalibration. The latest Artprice report confirms what many professionals have sensed intuitively over the past twelve months: the market is not collapsing, but it is changing pace, structure, and hierarchy. Headline figures may suggest contraction, yet beneath the surface, activity has never been broader nor more dynamic.

In 2024/25, auction turnover declined sharply, driven almost exclusively by the scarcity of trophy works and the retreat of ultra-high-end consignments. At the same time, transaction volumes reached record levels, revealing a market that is expanding at its base while concentrating value at its summit. This growing disconnect between volume and value has become one of the defining characteristics of the contemporary segment.

This report offers a clear snapshot of a market in transition: more global, more digital, more generational—and increasingly shaped by data, confidence, and selectivity. For collectors, dealers, and advisors, understanding these structural shifts is no longer optional. It is the difference between navigating the market with intuition alone—or with precision.

WORK IN PROGRESS

Key Takeaways from the Artprice Report

artprice.com, the world leader in Art market information

Global Overview

Turnover down, Transactions up

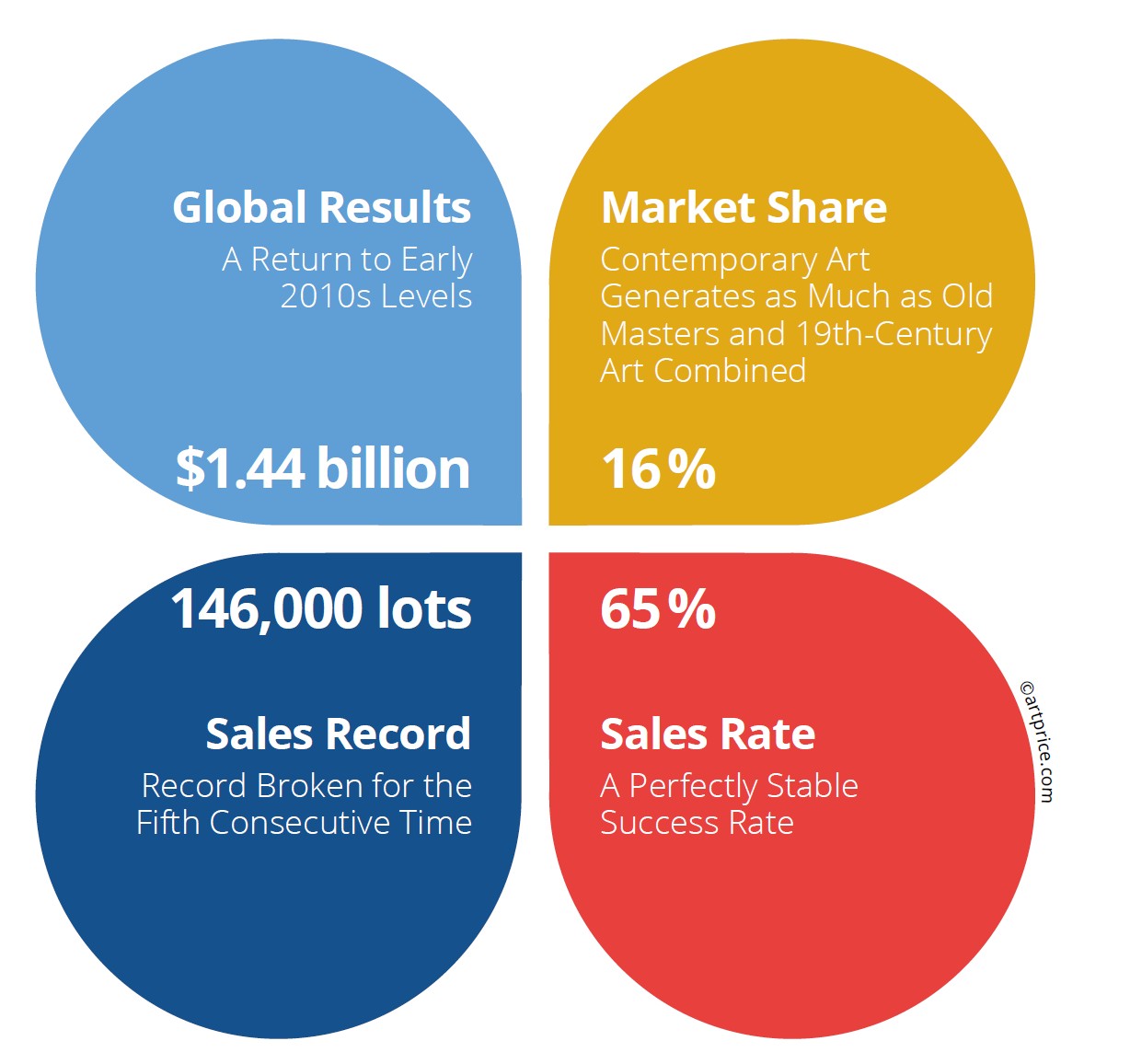

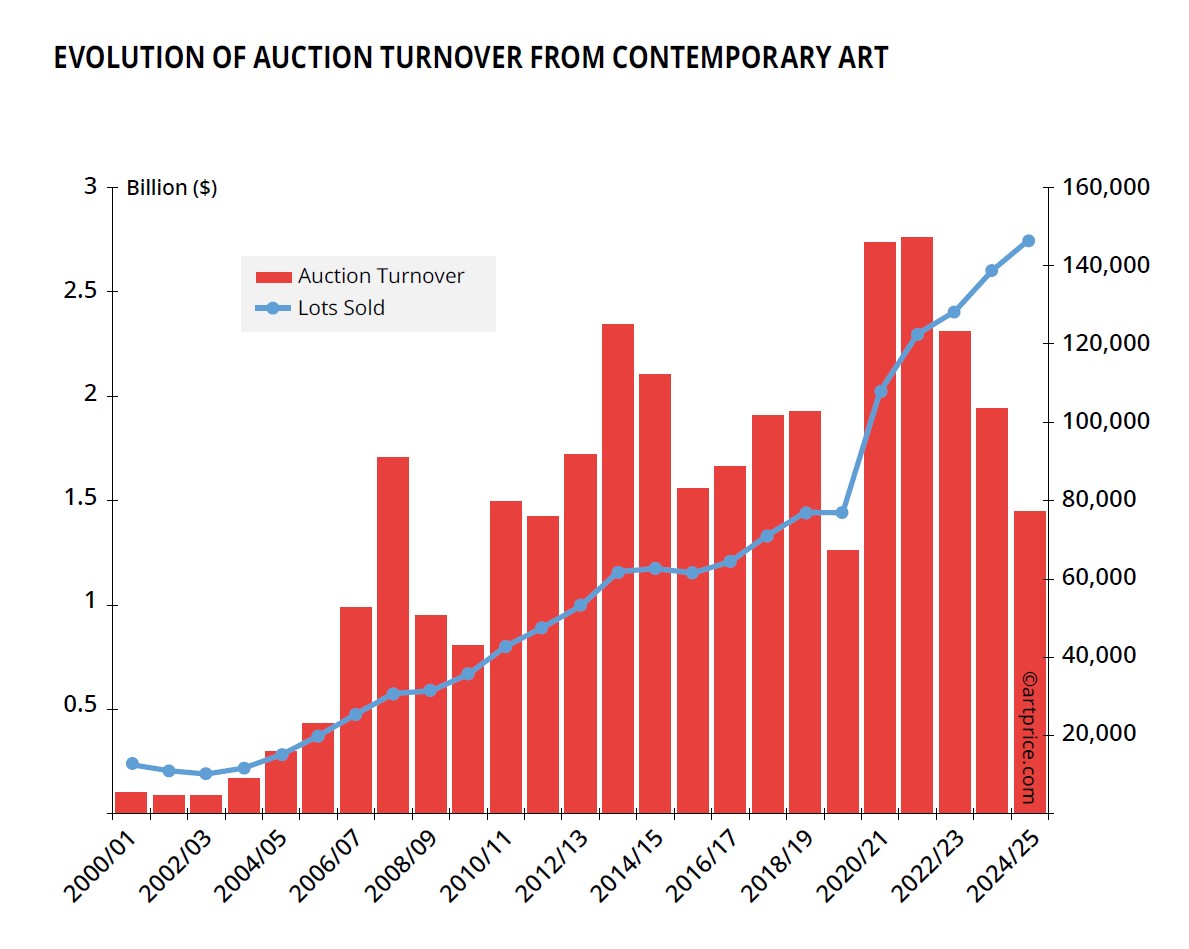

The global Contemporary Art auction market generated USD 1.44 billion in 2024/25, marking a 25% decline year-on-year and returning the market to early-2010s levels, after the exceptional post-Covid peak of 2021/22 (USD 2.75 billion). This contraction confirms a correction already visible since 2023, driven almost entirely by the slowdown in the premium segment rather than a collapse in demand.

At the same time, transaction volume reached an all-time record with approximately 146,000 lots sold, the fifth consecutive annual record. The Contemporary Art market is therefore not shrinking; it is rebalancing structurally, with volume expanding at the base while value contracts at the top.

A market with Two Speeds

Premium contraction vs. affordable expansion

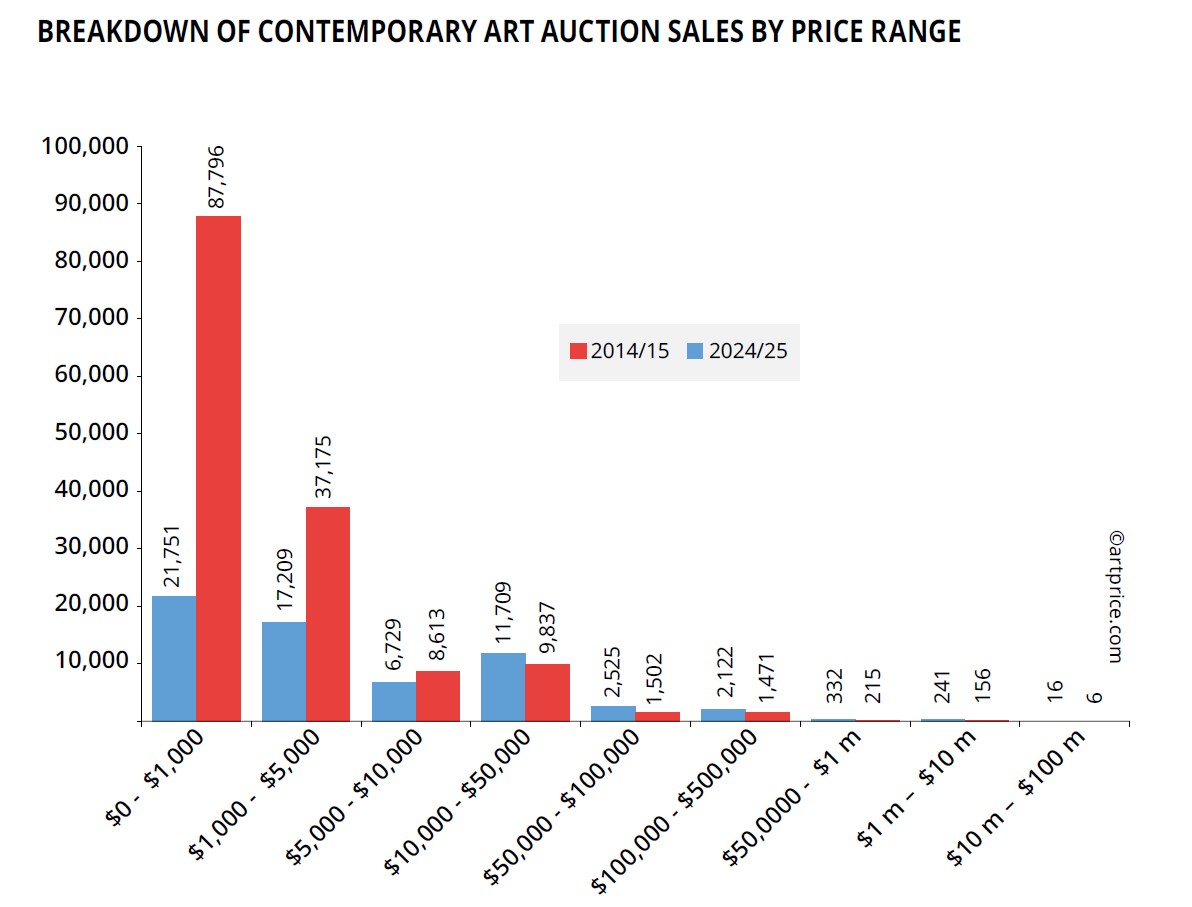

The defining feature of the year is a multi-speed market.

Works above $100,000 experienced the sharpest decline, with a 29% drop in million-dollar results, following an already severe contraction the previous year.

Works under $5,000 recorded a +9% increase in sales, now representing 85% of all transactions while accounting for just 8% of total value.

Conversely, lots above $500,000 represent only 0.3% of transactions, yet still generate 45% of total market value.

This imbalance between volume and value is structural and inherent to the art market, but in 2024/25 it became more visible than ever. The expansion of the affordable segment reflects the entry of new, younger collectors, increased online participation, and a shift toward lower-risk, pleasure-driven acquisitions.

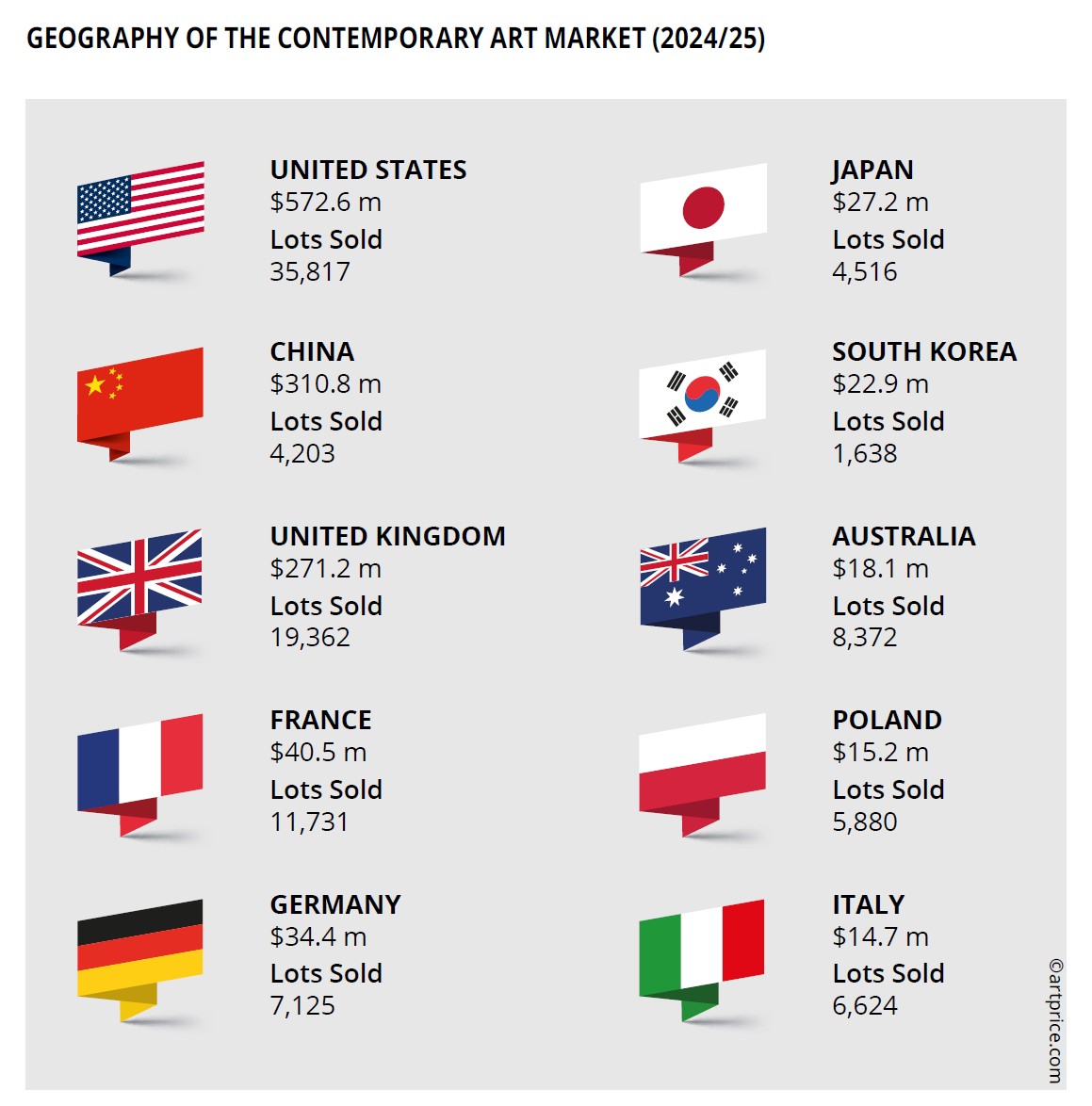

Geographic dynamics

The top contracts, Secondary markets rise

The United States, China, and the United Kingdom remain the core of the Contemporary Art auction market, accounting for 79% of global value with just 40% of total transactions. However, they also account for 92% of the global decline in turnover this year.

United States: $572.6 million (40% of global revenue), heavily impacted by the scarcity of prestige consignments.

China: $310.8 million (21.5%), with Hong Kong down 48%, marking its weakest performance in fifteen years.

United Kingdom: relatively resilient, down only 3% year-on-year, but still 33% below its ten-year average.

In contrast, Paris emerged as the world’s most dynamic marketplace by volume, with more contemporary works offered than New York, London, Hong Kong, and Beijing combined. France is now the fourth-largest market by value and Europe’s leading hub for Contemporary Art.

Beyond the major capitals, secondary markets such as Tokyo, Warsaw, and Copenhagen are gaining momentum, benefiting from digital infrastructure, regional collectors, and a strong supply of mid-priced works.

Supply, Confidence, and Private Sales

The downturn in turnover is not caused by a lack of wealth, but by psychological caution among collectors and sellers. Owners of major works are increasingly postponing consignments, while auction houses report that top-tier artworks now sell more effectively through private sales rather than in public rooms.

The result is a visible shortage of iconic works at auction, which mechanically depresses turnover even as demand remains intact for exceptional pieces. When such works do appear, buyers are still willing to commit significant sums, as demonstrated by seven-figure results across New York, Hong Kong, and Singapore.

Artists, Generations, and Buyer Behavior

More than 47,000 contemporary artists appeared at auction this year, with nearly 20% entering the auction market for the first time, confirming an unprecedented renewal of supply.

Generational change is now a decisive factor:

Millennials and Gen Z favor accessible price points (often below $10,000), online formats, prints, NFTs, and works engaging social or cultural themes.

Christie’s reports that 81% of bids in 2024 were placed online, with approximately one-third of buyers now under 40.

This shift explains the explosive growth in low-priced segments and the relative caution toward ultra-speculative ultra-contemporary names that surged during the post-Covid boom.

Artists: scale, renewal, and saturation

One of the most striking indicators in the 2024/25 report is the sheer scale of artistic supply. More than 47,000 contemporary artists appeared at auction during the year, with nearly 36,000 recording at least one sale, and close to one in five entering the auction market for the first time.

This constant renewal reflects a market that is not closing in on itself, but expanding horizontally. The infographic showing the growth in the number of artists and lots sold over the past two decades clearly illustrates this structural broadening of the contemporary segment, driven by digitalization, lower barriers to entry, and globalized access to auctions.

Female artists: visibility up, structural gap remains

Female artists continue to gain ground, particularly in terms of visibility, frequency of sales, and symbolic recognition. The report highlights a series of strong results, including new records for living female painters, confirming a gradual but tangible rebalancing.

However, the infographics comparing number of transactions versus total value make the situation explicit: while women artists are increasingly present in auction catalogs and sales volumes, their representation at the very top of the price spectrum remains limited. The evolution is real, but it is incremental rather than revolutionary, driven by consistent demand rather than sudden speculative spikes.

Ultra-Contemporary artists: correction after acceleration

The Ultra-Contemporary segment (artists under 40) illustrates the market’s current caution most clearly. After several years of rapid acceleration fueled by speculation and novelty, the number of very high-priced results has declined, particularly above the $500,000 and $1 million thresholds.

Artprice’s breakdown by price range shows that while transaction volume remains solid, buyers have become far more selective. Works perceived as overvalued or insufficiently anchored in institutional or gallery support are facing resistance, whereas artists with coherent trajectories and sustained backing continue to perform.

Icons vs. emerging names: consolidation rather than rotation

The report does not point to a radical shift away from established names, but rather to a consolidation of hierarchies. Major contemporary icons still dominate the top of the turnover rankings, even as their overall volumes soften. At the same time, a growing number of emerging and mid-career artists populate the lower and middle segments, absorbing most of the market’s transactional growth.

The relevant infographics show a market that is no longer driven by rapid rotations of “hot” names, but by durability, narrative clarity, and collector confidence.

Geographic influence on artists’ success

Artists’ auction performance is increasingly shaped by geographic ecosystems. The report highlights strong momentum for Japanese artists, particularly those supported by major international galleries, as well as the growing visibility of artists from secondary markets benefiting from local demand and digital reach.

Charts mapping artist performance by country and auction location reveal that success is no longer confined to New York or London alone, but increasingly distributed across Paris, Hong Kong, Tokyo, and other emerging hubs.

What the artist data ultimately reveals

Taken together, the artist-focused data paints a clear picture: the contemporary art market is less speculative, more selective, and more layered. Visibility is expanding faster than value, opportunity exists across a wider spectrum of practices, and long-term positioning now matters more than short-term hype.

For collectors and professionals, the infographics are unambiguous: understanding where an artist sits—by age, gender, geography, price range, and market depth—is now as important as understanding who the artist is.

Top Contemporary Art Auction Results

From 1 July 2024 to 30 June 2025

#1. Baby Boom, 1982

Christie’s New-York: 14 May 2025

Estimated: USD 20,000,000 – 30,000,000

USD 24,310,000

JEAN-MICHEL BASQUIAT (1960-1988), Baby Boom | Christie’s

REPEAT SALE

Phillips New-York: 13 May 2001

Estimated: USD 700,000 – 900,000

USD 1,160,000

JEAN-MICHEL BASQUIAT (1960-1988)

Baby Boom, 1982

Acrylic, oilstick and paper collage on canvas mounted on tied wood supports

49×84 inches (125 x 213.5 cm)

Signed, titled and dated ‘‘Baby Boom’ Jean-Michel Basquiat Aug. 1982’’ (on the reverse)

#2. Untitled, 1982

Christie’s New-York: 21 November 2024

Estimated: USD 20,000,000 – 30,000,000

USD 22,950,000

WORK ON PAPER

AUCTION RECORD FOR A DRAWING BY JEAN-MICHEL BASQUIAT

JEAN-MICHEL BASQUIAT (1960-1988), Untitled | Christie’s

JEAN-MICHEL BASQUIAT (1960-1988)

Untitled, 1982

Oilstick on paper

63 1/2 x 44 inches (161.3 x 111.8 cm)

Signed and dated ‘Jean-Michel Basquiat 1982’ (lower right)

USD 20 million

#3. Untitled, 1981

Sotheby’s New-York: 15 May 2025

Estimated: USD 10,000,000 – 15,000,000

USD 16,365,000

WORK ON PAPER

Untitled | The Now and Contemporary Evening Auction | 2025 | Sotheby’s

JEAN-MICHEL BASQUIAT (1960 – 1988)

Untitled, 1981

Oilstick on paper

50 1/4 x 63 7/8 inches (127.6 x 160 cm)

Signed (on the reverse)

#4. Sabado por la Noche (Saturday Night), 1984

Christie’s Hong-Kong: 28 March 2025

Estimated: HKD 95,000,000 – 125,000,000

HKD 112,625,000 / USD 14,476,221

Sabado por la Noche (Saturday Night)

REPEAT SALE

Christie’s London: 25 June 2019

Estimated: GBP 7,500,000 – 11,000,000

GBP 8,378,250 / USD 10,656,640

Jean-Michel Basquiat (1960-1988), Sabado por la Noche (Saturday Night) | Christie’s

JEAN-MICHEL BASQUIAT (1960-1988)

Sabado por la Noche (Saturday Night), 1984

Acrylic, silkscreen, oil stick, and paper collage on canvas

77×88 inches (195.6 x 223.5 cm)

Signed, titled, and dated ‘Jean Michel 1984 – “SABADO POR LA NOCHE”‘ (on the reverse)

#5. Miss January, 1997

Christie’s New-York: 14 May 2025

Estimated: USD 12,000,000 – 18,000,000

USD 13,635,000

AUCTION RECORD FOR A LIVING FEMALE ARTIST

MARLENE DUMAS (B. 1953), Miss January | Christie’s

MARLENE DUMAS (B. 1953)

Miss January, 1997

Oil on canvas

280×100 cm (110 1/4 x 39 3/8 inches)

Signed, titled and dated ‘M Dumas Miss January 1997’ (on the reverse)

#6. Cosmic Eyes (in the Milky Lake), 2005

Sotheby’s London: 5 March 2025

Estimated: GBP 6,000,000 – 8,000,000

GBP 9,027,500 / USD 11,555,200

READ MORE IN FOCUS SECTION

Cosmic Eyes (in the Milky Lake) | Modern & Contemporary Evening Auction | 2025 | Sotheby’s

YOSHITOMO NARA (b. 1959)

Cosmic Eyes (in the Milky Lake), 2005

Acrylic and glitter on canvas

162 x 130.2 cm (64 3/4 x 51 1/4 inches)

Signed, partially titled and dated 2005 (on the reverse)

#7. Balloon Monkey (Blue), 2006-2013

Christie’s London: 9 October 2024

Estimated: GBP 6,500,000 – 10,000,000

GBP 7,555,000 / USD 9,897,050

JEFF KOONS (B. 1955), Balloon Monkey (Blue) | Christie’s (christies.com)

JEFF KOONS (B. 1955)

Balloon Monkey (Blue), 2006-2013

Mirror-polished stainless steel with transparent color coating

150x126x235 inches (381 x 320 x 596.9 cm)

Executed in 2006-2013, this work is one of five unique versions (Red, Yellow, Blue, Magenta, Orange)

#9. Large Vase of Flowers, 1991

Christie’s New-York: 21 November 2024

Estimated: USD 6,000,000 – 8,000,000

USD 8,230,000

JEFF KOONS (B. 1955), Large Vase of Flowers | Christie’s

JEFF KOONS (B. 1955)

Large Vase of Flowers, 1991

Polychromed wood

52x43x43 inches (132.1 x 109.2 x 109.2 cm)

This work is the artist’s proof from an edition of three plus one artist’s proof

Strategic Takeaways

- The Contemporary Art market is adjusting, not collapsing.

- Liquidity has shifted decisively toward affordable works, expanding the collector base.

- Prestige and rarity remain the primary drivers of value at the top, but supply is currently constrained.

- Geographic leadership is fragmenting, benefiting secondary capitals and digitally agile markets.

- Information asymmetry remains high: data, context, and segmentation are now strategic assets, not optional tools.

The 2024/25 Contemporary Art market marks the end of a speculative cycle and the beginning of a more distributed, more democratic, and more data-driven ecosystem. Less spectacular in headline numbers, but broader, more resilient, and structurally healthier, it offers fertile ground for informed collectors, advisors, and platforms capable of transforming raw data into actionable intelligence.